The latest labour force data for the month of December were just released, the first of a few key indicators that are due to drop ahead of the Reserve Bank of Australia’s (RBA) next meeting on 18 February.

In this Hot Take I’m going to start with the employment numbers themselves, follow it up with a look at several indicators that were released since the last update, before wrapping up with what it might mean for inflation and interest rates.

By the numbers#

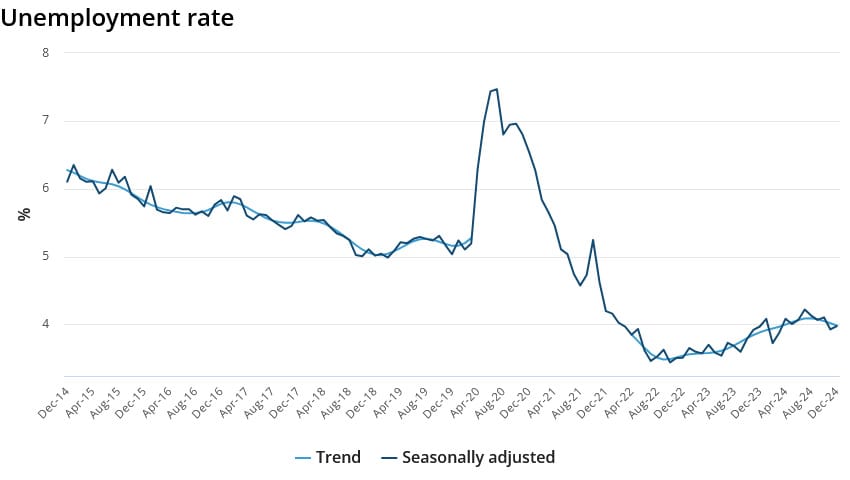

Australia’s unemployment and participation rates ticked up ever so slightly (0.1 percentage points) to 4.0% and 67.1%, respectively, in December. The trend continues to suggest a tightening of the labour market:

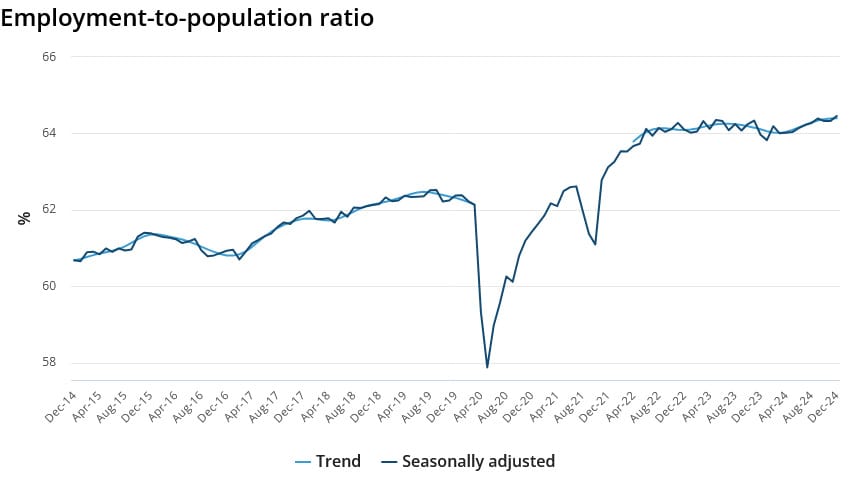

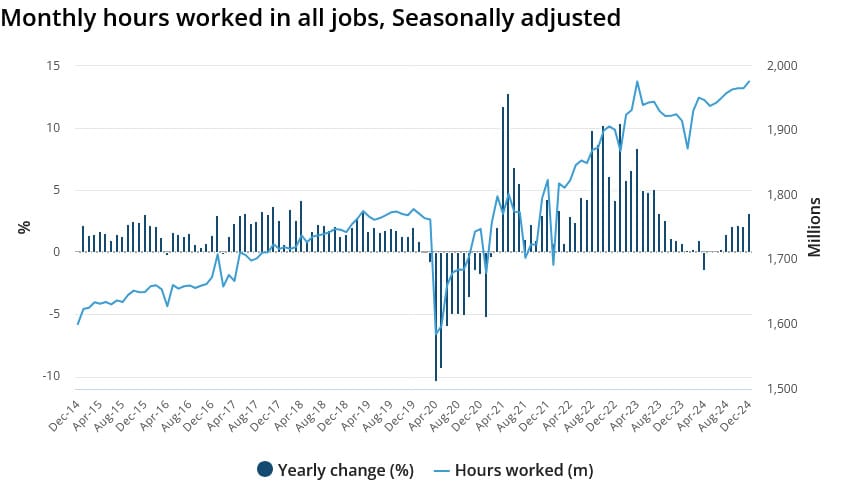

That’s supported by the employment-to-population ratio and hours worked, which both hit new highs:

These data mean that the RBA can rest easy about the full employment side of its dual mandate and focus on getting aggregate demand back down to Earth, with the forthcoming December quarter consumer price index (CPI) the last remaining piece of the puzzle.

Further context#

Since last week’s monthly CPI update a few official and market-based indicators were released, including retail sales, job vacancies, ANZ/Indeed job ads, and the Melbourne Institute’s monthly inflation gauge. Bond yields have also been moving across the world, with implications for the longer term inflation outlook.

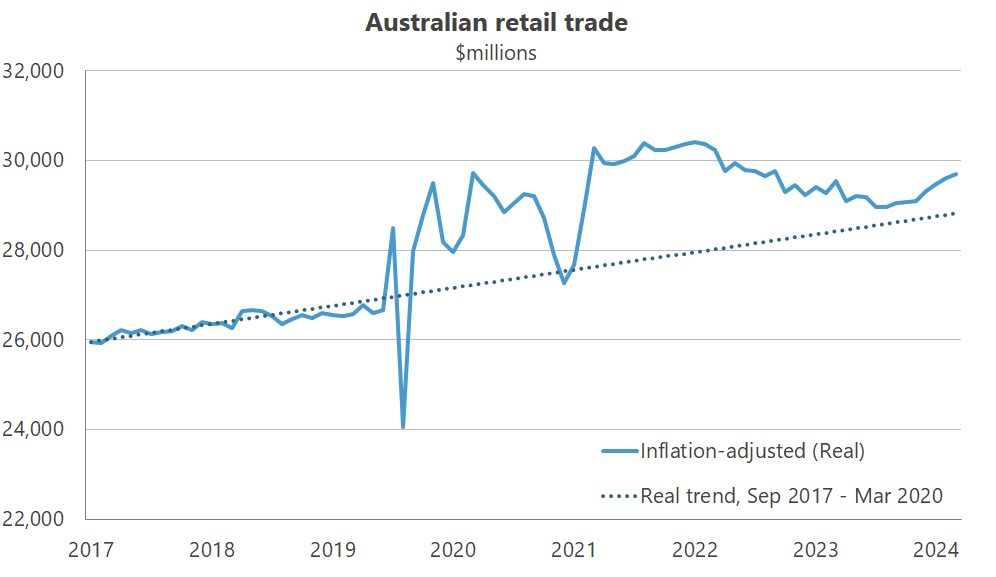

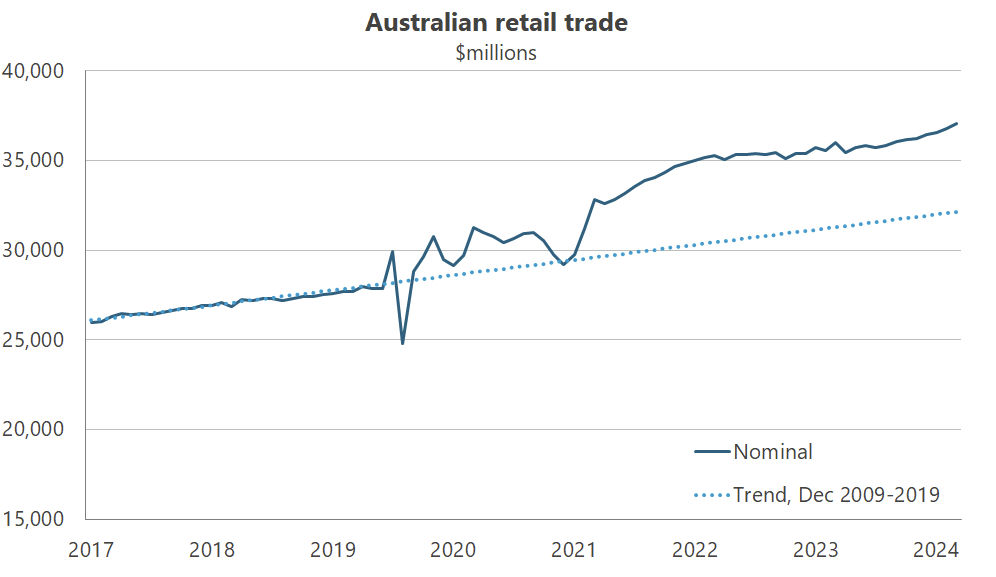

First up were retail sales, which picked up in November in both nominal and real terms.

If you were wondering whether aggregate demand is still too strong and putting upward pressure on inflation, that’s pretty solid evidence in the affirmative.

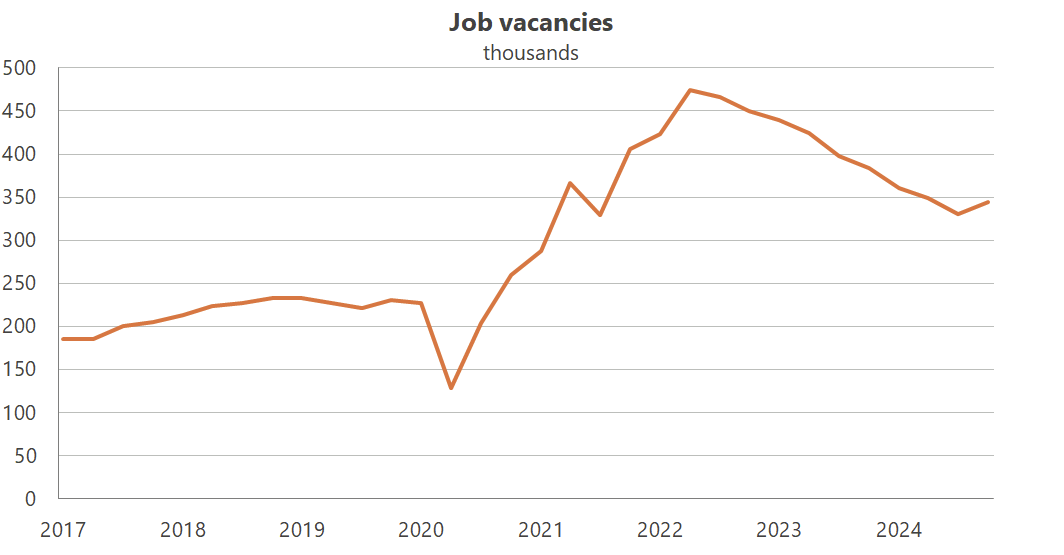

Moving on, there was further evidence of a tight labour market. Job vacancies rose, putting to end what was a long running trend back towards pre-pandemic levels. While Australia now has many more people than it did back in 2019 and this series doesn’t adjust for a growing labour market, it will give the RBA a bit of confidence that it can continue to focus solely on achieving its inflation mandate.

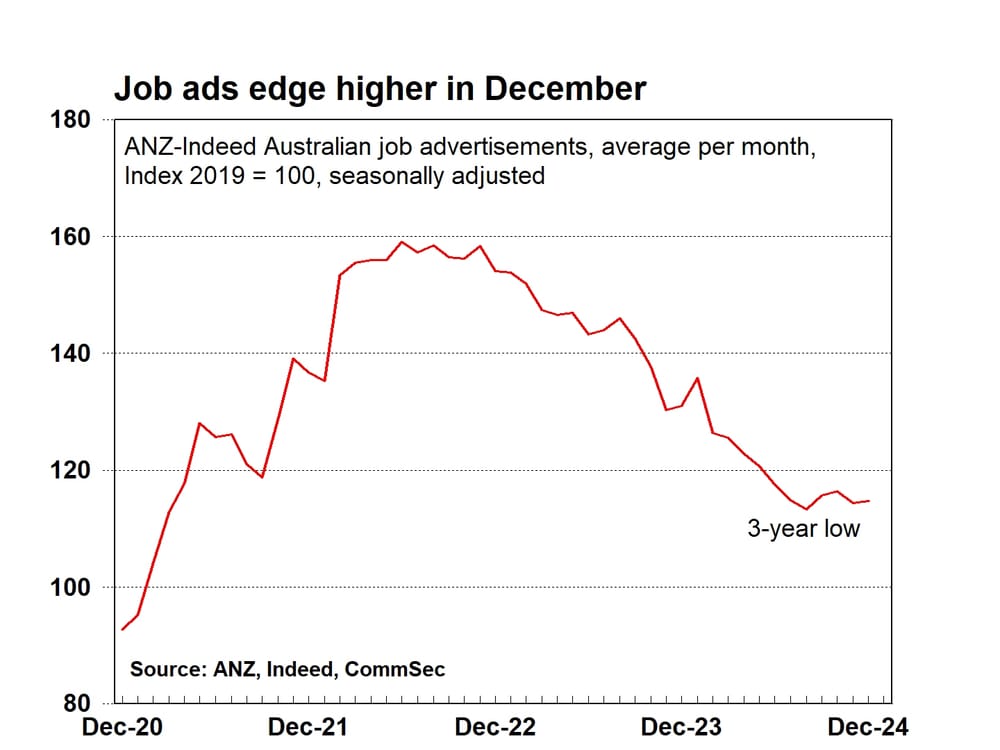

Still on the labour market, job ads were also stable at a 3-year low, with the level still 14.7% above pre-pandemic levels.

Then there was the Melbourne Institute’s monthly inflation gauge, which rose by 0.6% – the most in 12 months – while the trimmed mean version increased 0.4%, the most since March.

One caveat here: both gauges fell on an annual basis, suggesting there might be some seasonality (e.g. a late Black Friday in 2024) along with various subsidies coming on and rolling off causing a bit of mischief.

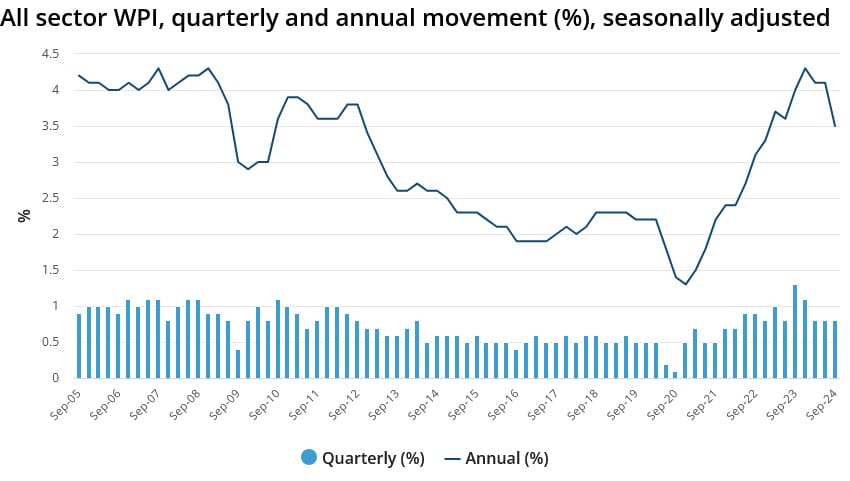

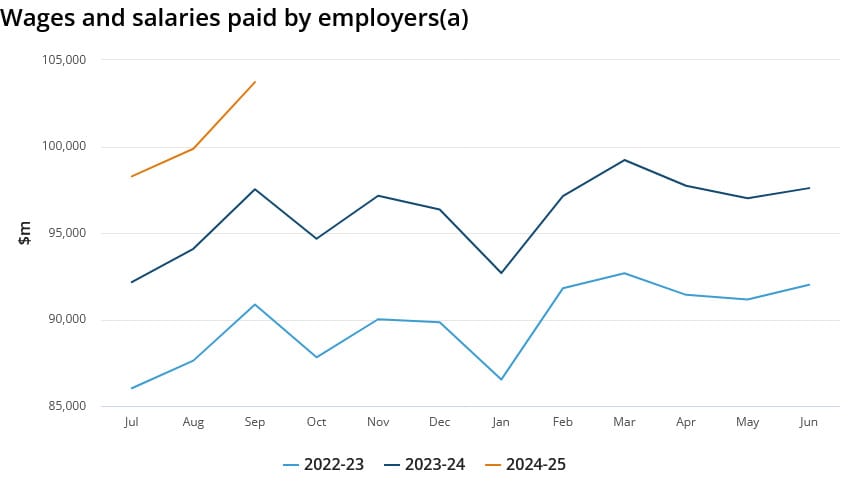

Next were nominal wages, which as of the September quarter were still growing at an annual rate of somewhere between 3.5% ( wage price index) and 6.3% ( single touch payroll). Both rates are high enough to put upward pressure on the RBA’s 2-3% inflation target, given zero productivity growth.

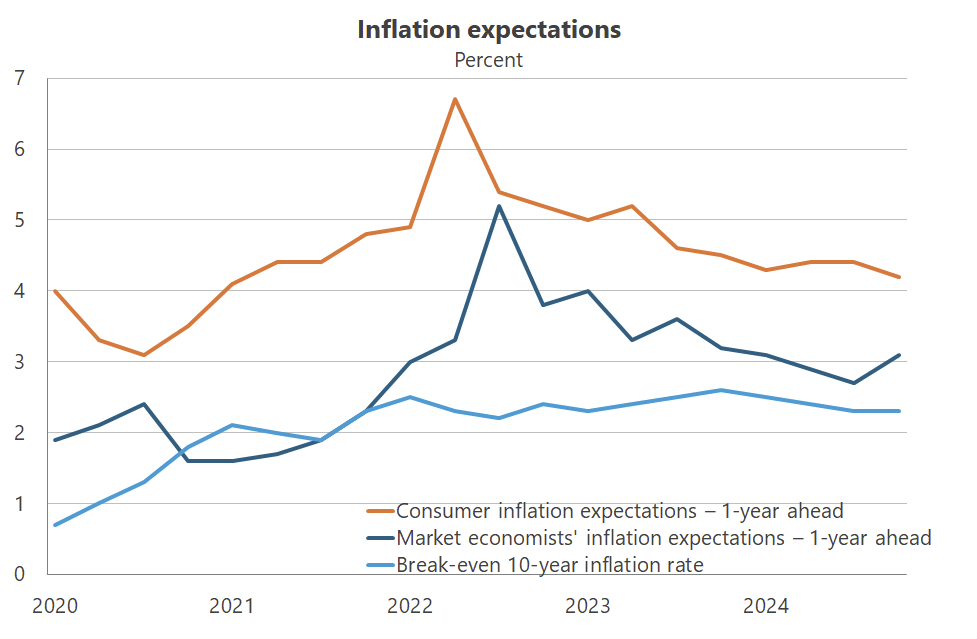

Finally, there was inflation expectations. Australian 10-year bond yields have continued to increase in recent months, and the nominal exchange rate continues to test new lows.

But both are incredibly difficult indicators to interpret, because there are many supply and demand factors beyond inflation that influence their movements. They’re also not that accurate; for example, bond markets completely failed to predict the recent inflation – it was consumers who noticed it first, and while the trend for those has come down in recent months, they’re still over 4%.

That said, research by Stanford economist Hanno Lustig has found that the bond market’s signals were being suppressed: quantitative easing, the fancy term used for large central bank purchases of government bonds, dulled the bond market’s pricing power for decades.

With central banks no longer buying bonds, private investors now have to absorb even more, pushing up yields and potentially restoring some of its ability to gauge future inflation.

But there’s still considerable uncertainty. After UK and US inflation surprised to the downside last night, bond yields fell across advanced economies, including in Australia. Basically, investors are looking for signs anywhere that the West might have conquered inflation, so I’d caution reading too much into them for now.

Wrapping up#

Monetary easing is coming, but I’m still not sold that the first rate cut will be in February, which will be the final meeting for the RBA’s existing board before the newly constituted monetary-specific policy board takes over. Today’s labour force data, combined with several other recently released indicators, only reinforce that view.

You have to remember that the RBA has been notoriously risk-averse and slow-moving in recent years. It will be wary of what has happened in the US, with the Fed cutting rates only for the labour market and inflation to prove sticky – so much so that there’s talk of no further cuts this year.

By the time the following meeting takes place on 1 April, the RBA will be armed with another monthly labour market reading, the December quarter’s CPI figures, and the national accounts. Only if those show progress on inflation, or employment worsens considerably, should it consider cutting rates.