Why the RBA should hold steady

When I was looking at the calendar a couple of weeks ago I had pencilled in the electoral bloodbath that looks set to take place in the UK tomorrow (sorry Rishi) as something to write about. But then Australia’s May inflation figures came in and I thought it warranted an update, given the relatively large upside surprise (market consensus was for 3.8%):

“The monthly CPI indicator rose 4.0% in the 12 months to May, up from a 3.6% rise in the 12 months to April.

The annual movement for the monthly CPI indicator excluding volatile items and holiday travel was also 4.0% in May, down from 4.1% in April. This series excludes Automotive fuel, Fruit and vegetables and Holiday travel and accommodation.

Annual trimmed mean inflation was 4.4% in May, up from 4.1% in April.”

The first thing to note is that this is the monthly inflation gauge; as I’ve documented before, it’s a series that “can be a bit tricky to interpret because of how our stats bureau cobbles it together”. Be careful reading too much into it.

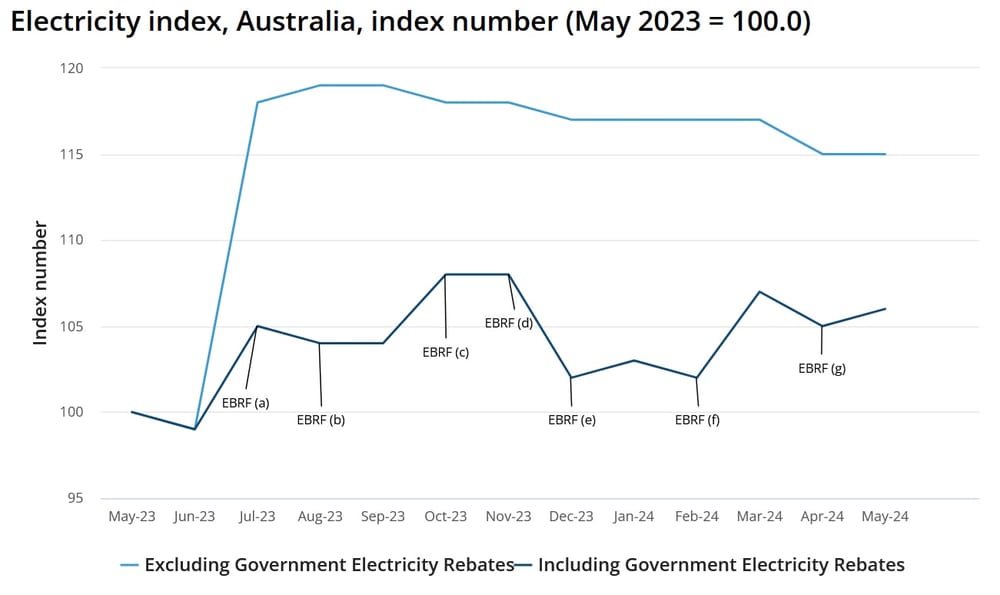

This month’s reading also contained a few so-called ‘base effects’, i.e., distortions from a year ago that have now dropped out. Government energy rebates are the primary culprit, as they temporarily lowered measured inflation. But because actual inflation hasn’t been reduced (if anything, by raising demand, debt-financed subsidies increase inflation), there’s an inevitable rebound effect 12-months later.

In May, the Energy Bill Relief Fund started to roll off the index, leading “to a 1.4% rise in Electricity prices in monthly terms” (up 6.5% from a year ago). And there’s plenty more to come:

The Reserve Bank of Australia (RBA) is, of course, well aware that these distortions need to be ’looked through’, and that the monthly indicators “don’t contain a full sample of prices”. Elaborating, Deputy Governor Andrew Hauser told an audience last week that:

“It would be a bad mistake to set policy on the basis of one number, and we don’t intend to do that.”

If I’m interpreting that correctly it means that barring a disastrous June quarter result, the RBA looks set to hold the cash rate steady at its next meeting in August (and probably many more).

But it’s also completely valid to ask that, given the utter lack of progress in getting inflation back to its 2-3% target – the last six readings excluding volatile items and holiday travel were 4.0, 4.1, 4.1, 3.9, 4.1, 4.2 – should the RBA be raising rates instead?

The case for higher rates

There’s a camp led by Christopher Joye that certainly thinks so:

“This column has warned ad nauseamthat excess demand across Australia, which is being powered by huge budget deficits at a time when labour markets are extremely tight, would fuel strong wage growth and services inflation, in turn underpinning unacceptably high consumer price pressures.

I’ve repeatedly asserted that the next move in rates should be higher, especially considering that the politicians are spending like mad men.

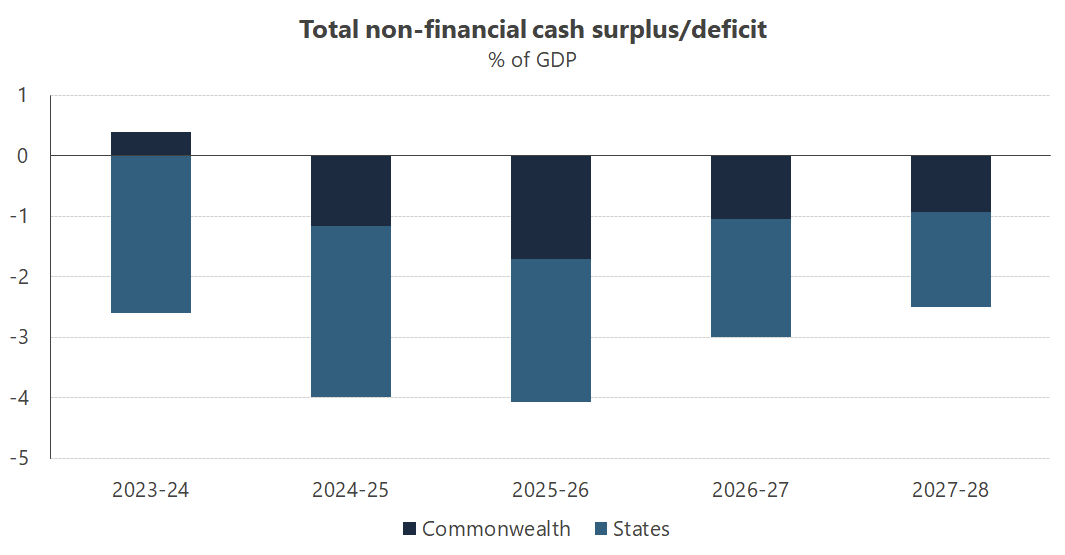

Deutsche Bank says that federal and state government deficits combined will be worth 3.6 per cent of GDP in 2024-25, up sharply from 2.1 per cent in 2023-24. So, when the politicians are meant to be constraining demand to help quell inflation, they are doing the opposite.”

I agree with Joye that our governments are making the RBA’s job a lot more difficult. For those who haven’t seen it, here’s my estimate of federal and state government deficits, which is a bit higher than the Deutsche Bank figure of 3.6% because I’m using underlying cash balances which also include their various “investments”:

There is no credible economic theory that supports such spending (sorry MMTers, that rules you out). Even the most ‘big government’ macro school, Keynesianism, argues that when demand is strong and unemployment is near a 50-year low, as it is in Australia, our governments should be reining in their spending:

“Keynesianism does not consist solely of deficit spending, since it recommends adjusting fiscal policies according to cyclical circumstances. An example of a counter-cyclical policy is raising taxes to cool the economy and to prevent inflation when there is abundant demand-side growth.”

So, our governments are doing their best to maintain inflation, despite their frequent doublespeak to the contrary. While inflation ultimately rests with the RBA, governments can make that task very hard to achieve because the cash rate is a blunt tool; without joint fiscal, monetary and economic reform, higher interest rates risk causing a recession followed by a rebound in inflation, because a weaker economy will inevitably lead to monetary easing and even more deficit-financed handouts from our governments. The cycle repeats.

The fiscal situation is precarious

Last week, the Parliamentary Budget Office (PBO) released its annual fiscal outlook, and it wasn’t pretty:

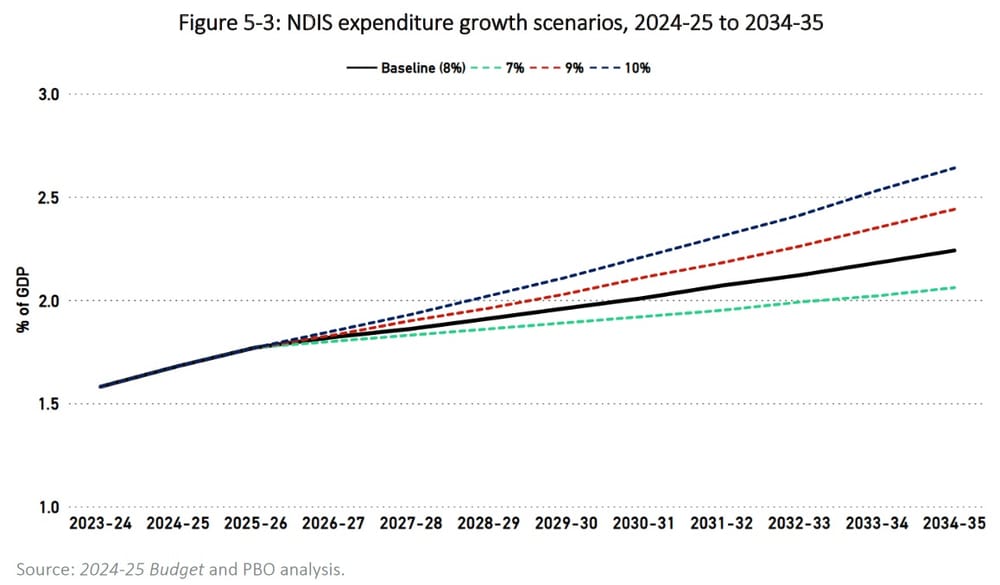

“Interest payments on Australian Government Securities are now projected to be the government’s fastest-growing major payment category between 2024-25 to 2034-35, with 9.9% average annual growth, displacing the NDIS as the fastest-growing payment in last year’s projections (9.2% average growth).”

By 2034-35, the PBO estimates that we’ll be paying about as much on the disabled as we are on national defence, even if Minister Shorten manages to limit its annual growth to 8% from the current ~20%, as he claims to be doing. But just a small 2 percentage point change to that growth rate will see NDIS expenditure compound to overtake defence prior to 2030:

Without spending reform – especially on entitlements such as the NDIS – our underlying fiscal problem will worsen, increasing the chances of inflation returning in the future.

But none of this is to say that the RBA is off the hook. Joye is absolutely correct that the cash rate should be higher, and that the RBA was both too late to start tightening and took too long to get rates to a reasonable level. It was pretty clear, several months into the pandemic, that the current crisis was not a 2008-style financial crisis/demand shock and did not warrant such an aggressive response.

But I disagree with Joye that rate hikes are needed from here.

The case against rate hikes

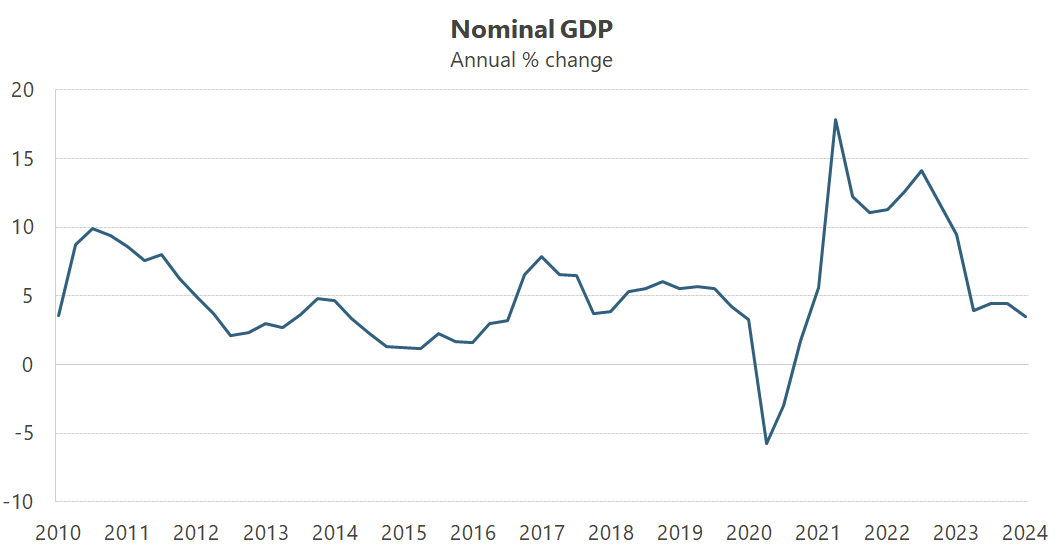

Nominal GDP, an indicator of aggregate demand – albeit less reliable in Australia because of the influence of global commodity prices, but an indicator nonetheless – is back to what might be considered ‘reasonable’ levels, after growing at rates not seen since the inflationary 1970-80 period for several quarters in 2021-22:

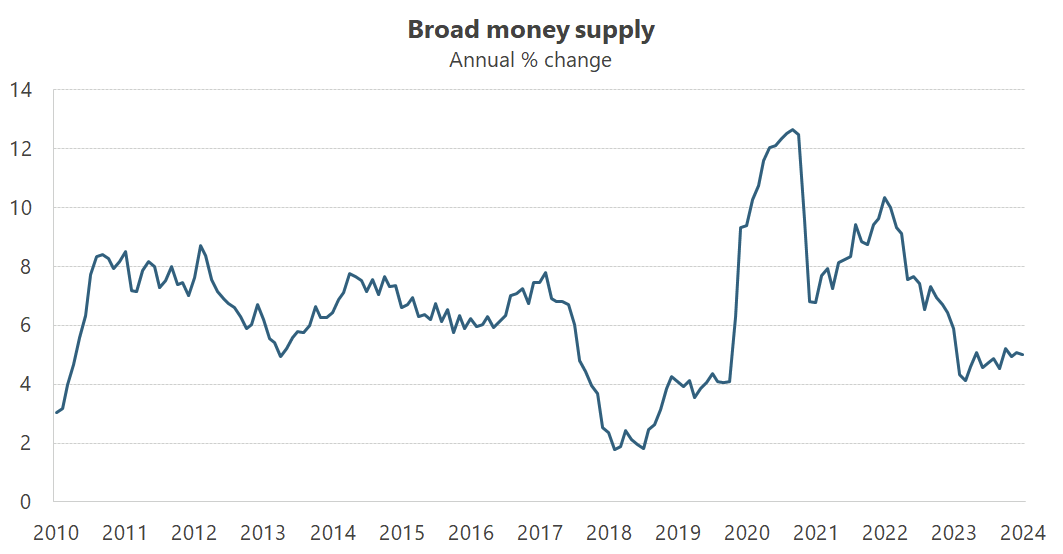

Similarly, after a surge during the pandemic, annual broad money growth has stabilised at around 5%:

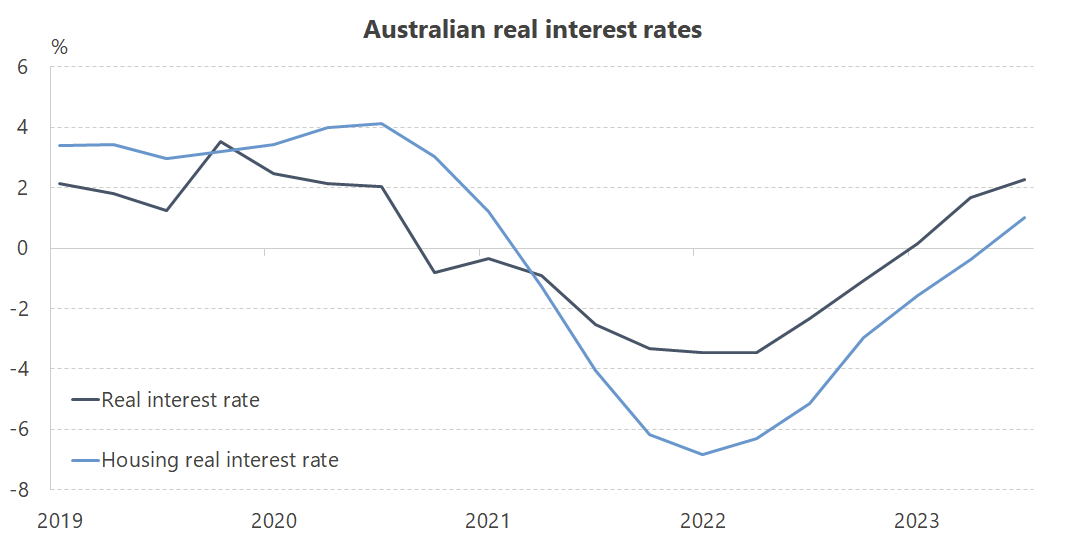

Real interest rates (even for housing) have now been positive for at least six months, which should be taking some sting out of demand:

While the RBA has been ‘on hold’ for several months, average rates on outstanding mortgages will keep increasing as many people fall off the ‘cliff’ of fixed- to variable- rate mortgages:

“According to [RBA economist Benjamin Ung], the avalanche of people paying higher mortgage rates mean that across all Australian households, total repayments will hit an all-time high of 10.5 per cent of disposable income by the end of the year [2024].”

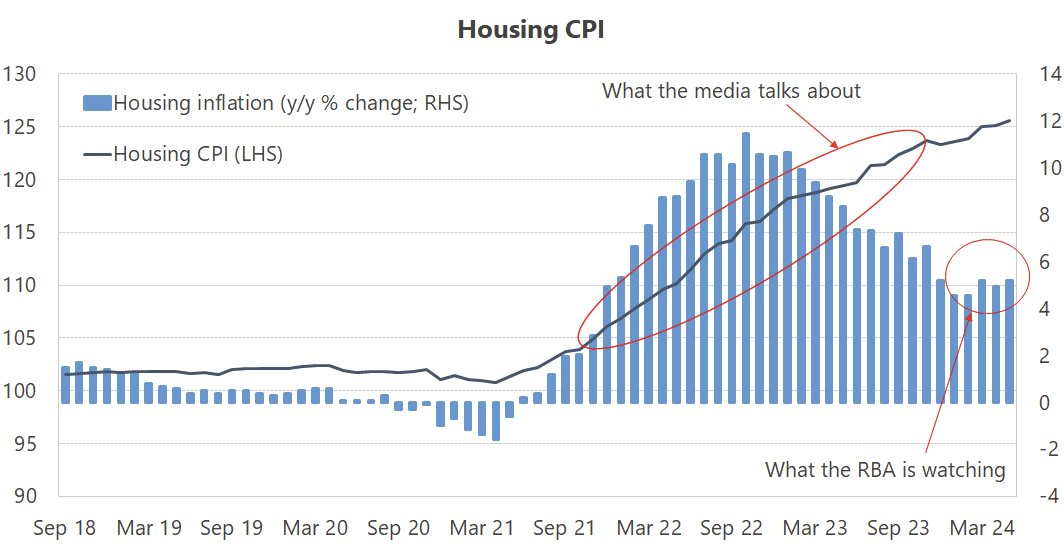

Additionally, much of the recent inflation has been driven by housing costs. But housing is somewhat lagged in the CPI, mostly because the rental component (up 7.4% in May) is a measure of the change in rent among all renters, many of whom aren’t renewing their lease when surveyed. Jarden’s chief economist, Carlos Cacho, reckons that the CPI lags asking rents by around 18 months. In May, asking rents in Australia’s capital cities fell 0.5%, “the largest percentage monthly decline in more than four years”.

While house prices are still rising, growth has slowed in the major markets of Sydney and Melbourne, suggesting there might be some downward pressure on the CPI’s housing component later this year. House prices might be up 45% since Jan 2019, but for inflation, what matters are the recent data points; everything that came before is baked in, and the RBA has no intention to reverse (deflate) that back to 2019 levels.

What all of this shows is that outside of housing (which is also being driven by supply constraints), the Australian economy is quite weak. Real GDP is growing at its slowest rate since 1991, and has been negative on a per capita basis for a year now. Despite the strong labour market, the Sahm rule – which is used (with mixed success) to predict recessions – is dangerously close to being triggered; in May it was just 0.12 percentage points off the 0.5 threshold.

In an ideal world, the RBA’s cash rate would have a 5 in front of it rather than the current 4. But that’s not the world we’re living in, and I think at this point the best path for the RBA is to hold steady. Any further rate rises will only really flow through in 2025 when we may already be in an outright recession.

The way out

On that note, for me the biggest risk is still stagflation: low growth and elevated inflation. And the RBA is partially responsible for that; by not tightening early enough and hard enough – by trying to walk the “narrow path” – it meant inflation stayed higher for longer, creating the conditions necessary for such an outcome by allowing inflationary expectations to rise, risking that they become entrenched, potentially even triggering a wage-price spiral.

At this point, with the nominal aggregates stable and a relatively weak economy, if inflation persists it’s likely going to be because of the lagged effects of excessive fiscal spending and nominal wage catch-up. There’s really not all that much the RBA can do about that without sucking demand out of the economy by causing a significant recession.

Yes, the RBA has done lasting damage to its credibility by being so slow to do its job, but I don’t think bringing forward a recession is going to do much to restore people’s faith in it. Really, what we need is tax, spending and regulatory reform. But the incentives are all wrong for that to happen:

“In particular, as explained by James Buchanan and Richard Wagner in their book ‘Democracy in Deficit,’ fiscal irresponsibility has a natural political advantage in democratic societies. Current generations reap the short-lived benefits of deficits—more government spending today—while future generations bear the burden but cannot vote. Ultimately, restoring fiscal responsibility will require the political will of lawmakers—and we citizens who elect them—to prioritise our posterity over ourselves.”

I’m a big fan of fiscal rules, especially for our state governments. The incentives are just too strong to do a bunch of short-term, politically-opportune stuff that screws the state over for many years to come. But I also recognise that surpluses are no longer as politically powerful as they were in the 90’s and 00’s, given many of today’s voters didn’t go through the 70’s and 80’s. No politician is going to agree to put a handbrake on their future spending ambitions with something like Switzerland’s debt brake if it won’t help them win an election.

But if our governments don’t cut back their spending – and this year’s budgets suggest they won’t – the only way out of our predicament is for meaningful reform to ignite economic growth, reducing deficits and inflationary pressures by outgrowing them. While I also don’t see that happening, a lot can change in a short amount of time; I’m not sure many people living in the 70’s and 80’s, when inflation was running in the double-digits, expected the neoliberal tide to sweep the world, ushering in unprecedented growth and 40 years of low inflation. But things might have to get worse before they get better.

Comments

Comments have been disabled and we're not sure if we'll ever turn them back on. If you have something you would like to contribute, please send Justin an email or hit up social media!